Average True Range Percentage

:max_bytes(150000):strip_icc()/ATR-5c535f8fc9e77c000102b6b1.png)

Average True Range Atr Definition

What Is Average True Range Fidelity

Average True Range Atr Chartschool

How To Use Average True Range True Trading Strategies Average

Moving Average Strategies For Forex Trading

True Strength Index Tsi Technical Indicators Indicators And Signals Tradingview

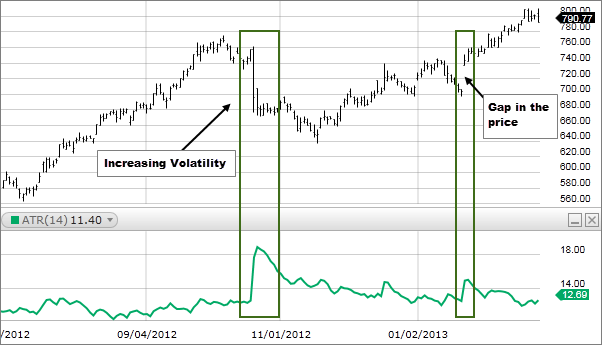

Usually the average true range atr is based on 14 periods and can be calculated on an intraday daily weekly or monthly basis.

Average true range percentage.

How To Download Install Atr Indicator For Mt4 And Mt5

Scalping Forex Scalpingforex Forex Forex Trading System Binary

Choppiness Index Indicator Trading Strategy Stockmaniacs Trading Strategies Cryptocurrency Trading Trend Trading

Make 98 Profit Only In 30 Seconds Too Good To Be True With This Website You Can Trade And Make Easy Mercado De Acoes Investimento Investimento Financeiro

Source : pinterest.com